Asset, Financial and Earnings Situation

BALANCE SHEET STRUCTURE

The unbroken strength of our new business results led to an increase in total assets which rose from € 38.1 billion on 31 December 2015 to € 38.5 billion at the end of 2016.

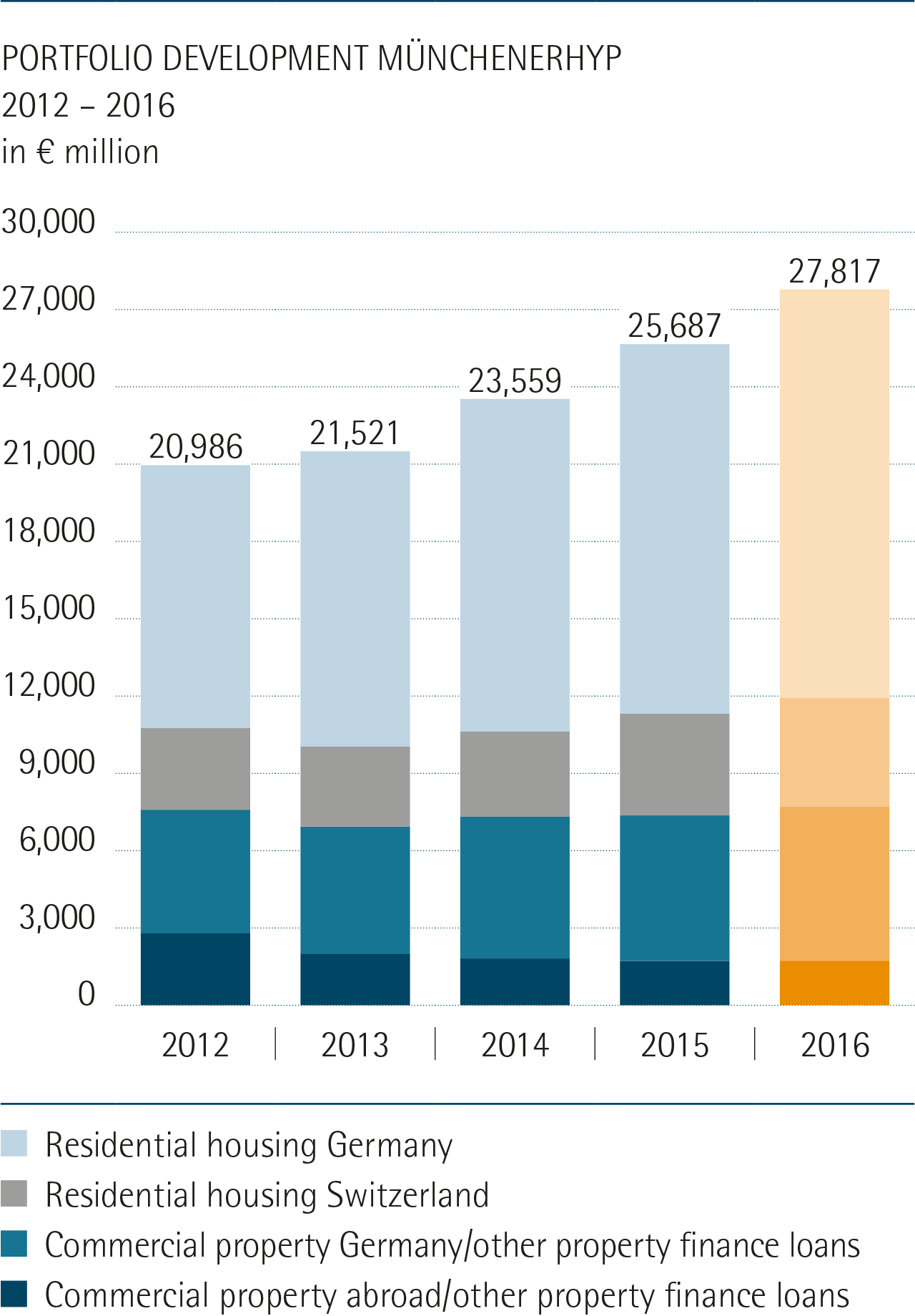

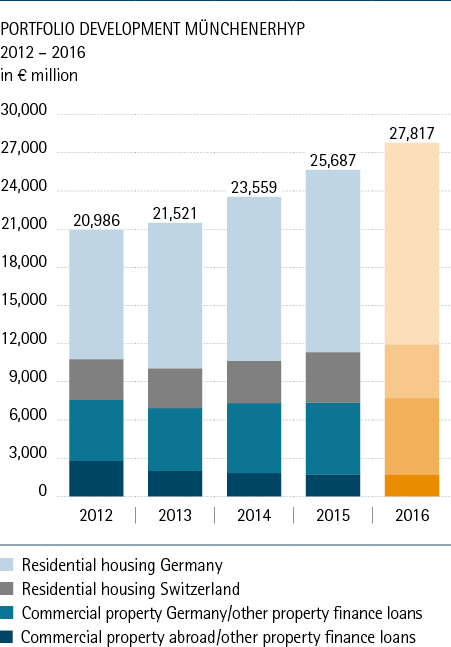

During the course of the year our mortgage loan portfolio grew by € 2.2 billion to € 27.8 billion.

Private residential property loans were once again the strongest growing area of business and increased by € 1.8 billion.

Our portfolio of private residential property loans is structured as follows: domestic mortgage loans € 15.9 billion (previous year € 14.4 billion), foreign mortgage loans € 4.2 billion (previous year € 3.9 billion), which were solely loans made to finance residential property in Switzerland.

Our portfolio of commercial property loans amounted to € 7.7 billion (previous year € 7.3 billion), of which € 1.7 billion (previous year € 1.7 billion) represented loans made outside of Germany. Property we financed in the USA accounted for 13 percent (previous year 22 percent) of the total, with EU countries accounting for the remainder.

In accordance with our business and risk strategy, our portfolio of loans and securities related to our business with the public-sector and banks declined further from € 8.2 billion to € 6.8 billion, of which € 2.9 billion were securities and bonds.

At the end of 2016 the net sum of unrealised losses and unrealised gains in our securities portfolio amounted to plus € 41 million (previous year plus € 34 million). These figures include unrealised losses of € 6 million (previous year € 10 million) stemming from securities issued by countries located on the periphery of the euro area and banks domiciled in these countries. The total volume of these securities amounted to € 0.6 billion (previous year € 0.9 billion).

Following a detailed examination of all securities we came to the conclusion that no permanent reductions in value are required.

We are keeping these bonds on our books with the intention of holding them until they mature. Write-downs to a lower fair value were not necessary.

The portfolio of long-term refinancing funds increased by € 0.6 billion to € 32.7 billion, of which € 20.3 billion consisted of Mortgage Pfandbriefe, € 4.7 billion of Public Pfandbriefe and € 7.7 billion of unsecured bonds. The total volume of refinancing funds – including money market funds – rose from € 35.4 billion in the previous year to € 35.8 billion on 31 December 2016.

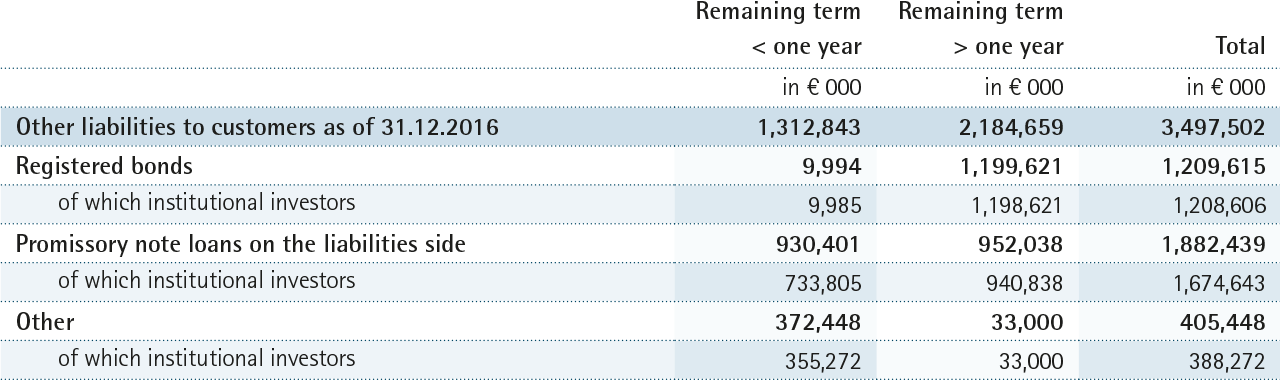

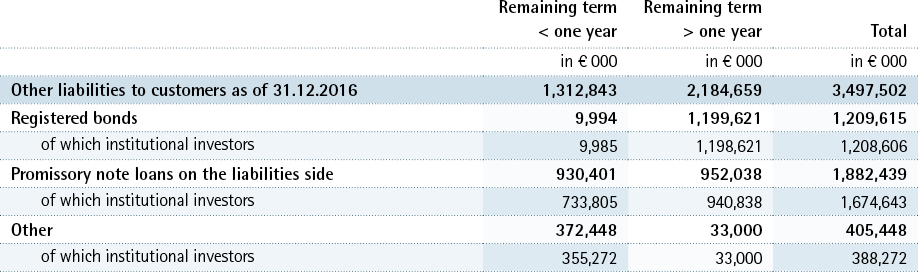

The item “Other liabilities to customers” is structured as follows:

Paid-up capital increased by € 250.7 million to € 956.0 million. Total regulatory equity capital amounted to € 1,343.1 million (previous year: € 1,372.0 million) and was slightly below the previous year’s figure. The reduction does not affect the elements which count towards Common Equity Tier 1 capital.

Our Common Equity Tier 1 capital increased from € 979.6 million in the previous year to € 1,251.3 million. On 31 December 2016 the Common Equity Tier 1 capital ratio was 22.9 percent (previous year 17.3 percent), the Tier 1 capital ratio was also 22.9 percent (previous year 19.5 percent) and the total capital ratio was 24.5 percent (previous year 24.2 percent). The leverage ratio was 3.35 percent on 31 December 2016.