Overall Economic Conditions

FINANCIAL MARKETS

Financial markets in 2016 were influenced by the political successes scored by populist movements, as well as the increasing divergence in monetary policies pursued by central banks in mature economies. The results of the Brexit referendum led to a massive decline in stock prices for a short period as a majority of market players had expected a “remain” victory. Donald Trump’s election as president of the USA also resulted in a sharp reaction as the bond market posted losses while equities gained. In contrast, the market’s reaction to the failed Italian referendum to reform the constitution was far more moderate.

Different rates of economic growth and inflation in developed economies led to a divergence in monetary policies pursued by the European Central Bank (ECB), the Bank of England and the Bank of Japan, on the one hand, from the policy followed by the American Federal Reserve (Fed), on the other hand. The ECB embraced a very loose monetary policy to strengthen inflation and avoid the dangers of deflation. For this reason, it lowered its interest rate on main refinancing operations by 5 basis points in March 2016 to 0 percent and its deposit facility rate by 10 basis points to minus 0.40 percent. In addition, it expanded its monthly asset purchase programme by an additional € 20 billion to € 80 billion. The Bank of England – in response to the Brexit vote – as well as the Bank of Japan – to counter low inflation and weak economic growth – also retained their expansive monetary policies. In view of improved economic data and lower unemployment in the USA, the Fed, in contrast, increased its key interest rate by 25 basis points in December 2016 to the range of 0.50 percent to 0.75 percent. Among other things, the difference in yield between ten-year German Bunds and US Treasuries widened to 166 basis points at the end of the year.

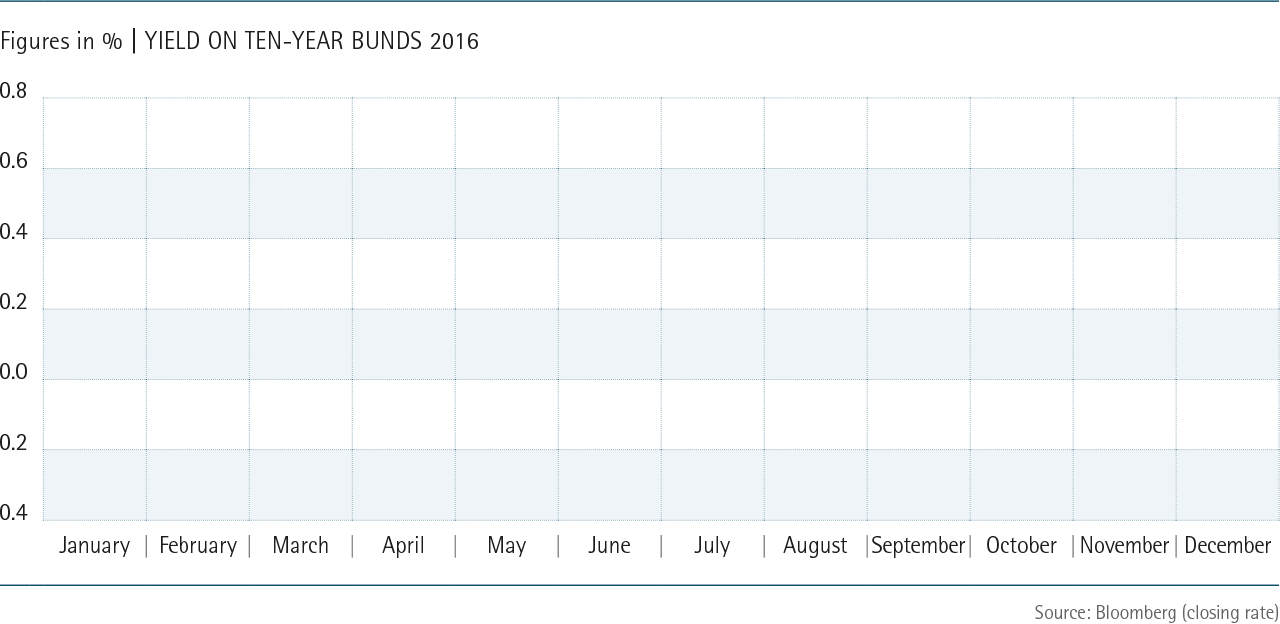

The ECB’s policy led to further declines in spreads and yields in the bond market. Economic development in the euro area was expected to weaken further at mid-year due to the Brexit decision. As a result, the yield on the 10-year Bund to hit a new historic low of minus 0.205 percent. Over the remaining course of the year higher oil prices as well as favourable economic data in the UK, plus statements made by the newly elected American president regarding financial policy, raised expectations for economic growth and inflation, which led to a rebound in yields. At the end of the year 10-year Bunds were yielding plus 0.20 percent.

The stock markets once again experienced greater volatility as the DAX lost almost 20 percent in the first weeks of the year only to recover and then rapidly decline again following the Brexit vote. The DAX went on to stabilise and rise sharply following the election of Donald Trump through to the end of the year. DAX rose by about 7 percent to the end of 2016 compared to its start in January and closed out the year at almost 11,500 points. The Dow Jones index also had a weak start but was able to make up for initial losses over the course of the year. The results of the presidential election in the USA also drove a notable rise in the Dow Jones in the remaining weeks of the year.

The US dollar was able to gain in the foreign exchange markets during the year. The gains were driven by improved economic data in the USA in the third quarter of 2016, as well as the newly elected president’s announced plans to expand fiscal policy and spending. The fact that the Fed was pursuing a more restrictive monetary policy than the ECB also helped to raise the value of the dollar. The US dollar spent most of the year in a range of 1.08 to 1.14 to the euro. The rate only made a major move higher for the US dollar in the fourth quarter when it became increasingly apparent that interest rates were going to rise in the USA. Towards the end of the year the dollar stood at 1.04 to the euro, the highest it had been in 14 years. The Brexit decision placed a heavy burden on the British pound as it lost value against all major currencies. This led the Bank of England to lower interest rates in response to the Brexit vote and to increase the volume of its bond purchase programme. These steps restored a certain level of stability. In addition, economic data did not develop as weakly as had been feared following the Brexit vote. At its low point the pound lost about 20 percent to the euro. At the end of the year the pound was quoted at 0.85 to the euro, or about 15 percent lower than at the start of year. The Swiss franc remained at a relatively stable rate vis-à-vis the euro and closed out the year at 1.07 CHF to the euro.

The ECB remained the main driver of activity in the covered bond markets as it bought more than one-third of all benchmark covered bond issues as part of its Covered Bond Purchase Programme (CBPP 3). Although traditional investors, like banks, insurance companies and investment funds, remained present as buyers in the market, the ECB’s purchases pushed them further to the sidelines. In addition, the low level of interest rates and spreads also reduced their willingness to build new positions. At the same time, high ratings and regulatory preferences associated with covered bonds and Pfandbriefe continued to make them favoured investments.

The volume of new issues declined due to the ECB’s longer term financing operations, and regulatory pressures on banks to lower the volume of low-margin public-sector loans on their balance sheets. Furthermore, issuing activities also declined due to political uncertainties. However, the year’s issuing activities got off to a stronger start than in the previous year. About three quarters of the total volume of new benchmark covered bonds were issued in the first half of the year. Total issuing activities did not, however, meet the market’s expectations as total volume fell from € 145 billion in 2015 to € 127 billion. As in the previous year, German Pfandbriefe, with € 24 billion in new issues, held the lion’s share of new issues, followed by French covered bonds with € 21.6 billion and Spanish Cedulas with € 13.5 billion.